For years, too many buyers treated power resilience like an insurance policy they could shop for later. That era is over. The current U.S.-Israel war with Iran and the risk surrounding the Strait of Hormuz are forcing the market to remember a very old lesson: when fuel routes are under pressure and electricity demand keeps climbing, immediate access to power equipment becomes a strategic advantage, not a convenience.

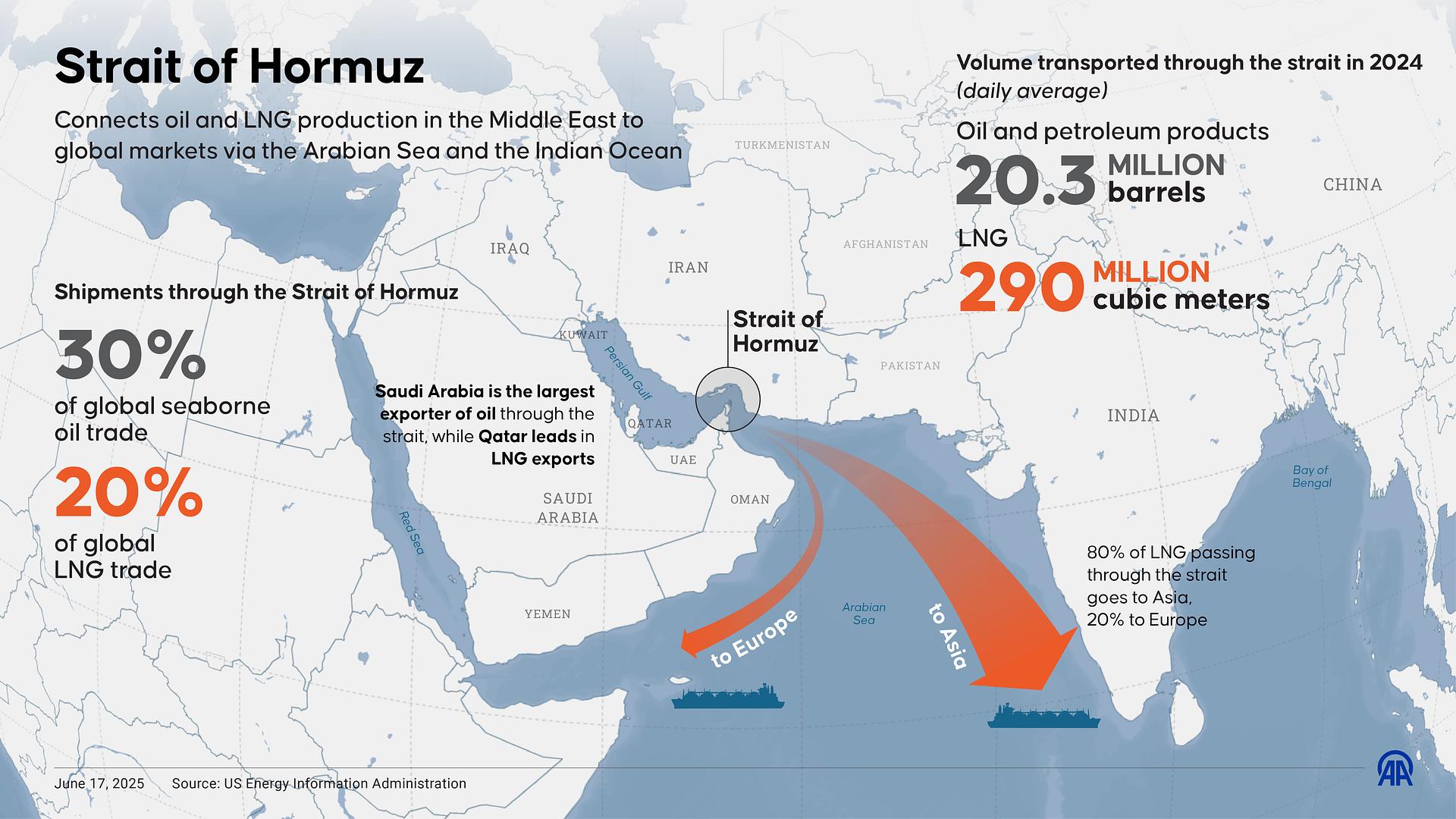

The Strait of Hormuz is not some abstract geopolitical talking point. It is one of the most important energy chokepoints on earth. EIA says it moved about 20 million barrels per day in 2024, representing about 20% of global petroleum liquids consumption, more than one-quarter of global seaborne oil trade, and around 20% of global LNG trade. EIA also notes there are only limited alternatives to bypass the strait, with roughly 2.6 million b/d of spare Saudi and UAE pipeline bypass capacity available in a disruption scenario. In plain English: if Hormuz is constrained, the world does not simply shrug and reroute everything overnight.

That matters because the world is already entering a period of structurally higher electricity demand. The IEA expects global electricity demand to grow by an average 3.6% per year from 2026 to 2030, adding roughly 1,100 TWh each year. In the United States, the EIA says electricity demand is on track for its strongest four-year growth period since 2000, driven largely by large computing facilities and data centers. The IEA also projects U.S. electricity use to add more than 420 TWh over the next five years, with about half of that growth tied to data centers.

This is the point many people still miss: geopolitical energy risk and AI-era electricity demand are colliding at the same time. The issue is no longer just oil. It is power density, speed to energization, transformer availability, fuel flexibility, and whether critical facilities can secure dependable megawatts without waiting 12, 18, or 30 months. The IEA projects global data-center electricity consumption to reach about 945 TWh by 2030, nearly double current levels, while Reuters reports developers are planning tens of gigawatts of on-site power and co-located generation to deal with grid constraints and speed-to-power pressure.

My view is simple: buyers waiting for “normal” conditions are making a bad bet.

When a fuel chokepoint is under threat, when oil and LNG logistics are strained, and when utilities are already dealing with rising load, the value of dispatchable equipment rises fast. Not theoretical equipment. Not brochure equipment. Available equipment. Equipment that can be inspected, transacted, shipped, installed, and put to work. That is where real market leverage sits.

That is also why the most relevant parts of today’s power market are not limited to utility-scale generation. They include fast-deployable industrial generators, Tier 4 Final units for regulated sites, transformer inventory that can keep projects moving, and larger turbine assets for buyers thinking beyond temporary backup and toward serious generation capacity. ARC Power Systems is positioned in exactly that lane.

For buyers needing substantial, modern standby or prime-capable capacity, these 2022 Cummins DQGAS QSK50-G8 1500kW Tier 4 Final units offer surplus-new condition, factory-test-hour status, 277/480V output, and integrated aftertreatment. For buyers needing compliant 1 MW-class capacity for data-center support, industrial standby, or permitted sites, these 2022 Cummins DQFAH 1000kW Tier 4 Final generators are already positioned around exactly that use case.

If the requirement is proven diesel capacity with fast deployment value, the 2014 Caterpillar C32 1000kW diesel generator set deserves attention. And if the constraint is upstream electrical infrastructure rather than generation alone, the 2022 Eaton 2600 kVA pad-mounted transformers are highly relevant because immediate transformer availability is now a competitive edge in its own right. ARC’s current Eaton listing emphasizes immediate availability, 34.5kV primary to 416Y/240V secondary, and a 3-year warranty—exactly the kind of practical infrastructure that keeps projects from stalling.

And for buyers operating at a completely different scale, the conversation naturally expands to larger generation blocks such as these Westinghouse 501B gas turbines. ARC’s listing identifies them as dual-fuel 73 MW-class machines. In a market that is rediscovering the importance of firm, dispatchable generation, large-frame turbine assets should not be treated like niche inventory. They are strategic assets.

The big mistake in this market is assuming the only story is higher fuel prices. It is bigger than that. Reuters reports energy executives are warning that the Iran conflict can damage broader supply chains, not just oil balances. That matters for semiconductor supply, industrial production, project schedules, and cost certainty. When buyers see that kind of instability, they start valuing speed, certainty, and available megawatts more aggressively than they did in softer markets.

So here is the opinionated version: the power market is done rewarding procrastination.

If you are building a data-center project, expanding industrial load, replacing aging standby infrastructure, or trying to secure generation before the next supply shock, waiting for “better timing” is not a strategy. It is exposure. The right strategy is to secure equipment that already exists, fits the application, and can move on real-world timelines.

That is where ARC Power Systems comes in. We focus on the part of the market that matters most when conditions tighten: real equipment, real capacity, and real availability. You can browse our full inventory here, or contact us directly if your project requires anything from rental-grade mobile generation to data-center-class backup systems, transformers, or utility-scale turbine assets.

In markets like this, the winners are rarely the people who waited for calm. They are the people who secured power before everyone else realized they needed it.

FAQ's

Why does the Strait of Hormuz matter to generator buyers?

Because it is one of the world’s most important oil and LNG chokepoints. Disruptions there can raise fuel costs, strain logistics, and make reliable on-site power more valuable.

Is this only an oil story?

No. It is also a power-security story. Rising data-center load, grid constraints, and longer infrastructure lead times mean reliable dispatchable power matters more than before.

Why are transformers part of this conversation?

Because generation alone does not energize a site. Projects also need the right electrical infrastructure, and immediate transformer availability can eliminate major schedule risk. ARC currently lists 2022 Eaton 2600 kVA pad-mounted units with immediate availability.

Are diesel generators still relevant in 2026?

Yes. For standby, rapid deployment, mobile power, and regulated-site applications, diesel remains a core solution, especially when buyers need dependable equipment now rather than theoretical future capacity. ARC’s current Cummins and Caterpillar listings reflect that reality.

What kind of buyers should be paying attention right now?

Data centers, industrial facilities, hospitals, utilities, EPCs, municipalities, and any project team facing energization risk, load growth, or long OEM lead times.

📞 Office: (213) 371-2848

📧 Email: sales@arcpowersystems.com

🌐 Website: www.arcpowersystems.com